A new look at the bullwhip effect in supply networks

New research updates one of the most well-known theories in supply chain management for a networked world

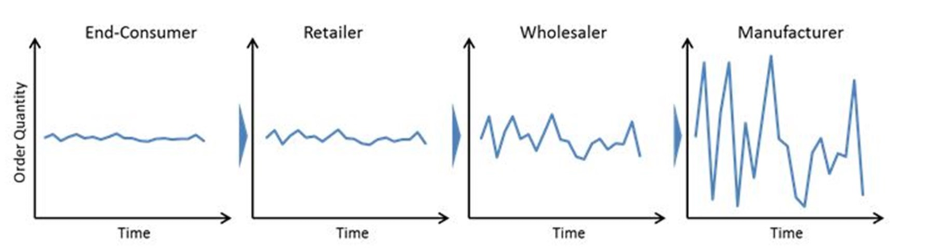

The bullwhip effect (BWE) is one of the most important ideas in operations management. First publicized by researchers Hau L. Lee, V. Padmanabhan, and Seungjin Whang in an MIT Sloan Management Review article in 1997, the hypothesis has become something every student of supply chains must understand. As illustrated in Figure 1 below, BWE refers to a situation in which naturally occurring product demand volatility at the end-consumer level is magnified by each stage of the product's supply chain. When BWE is present, the consumer's decisions reverberate all the way to the last stage of the supply chain, with volatility increasing at each step of the way.

Figure 1: The “bullwhip effect” as demand volatility increased upstream in the supply chain. (Source: IMD)

There are endless articles, papers, and even YouTube videos about BWE, and a common feature of the literature is that the phenomenon is described from the point of view of a single sequence from customer to retailer to manufacturer to supplier(s), i.e., as an "intra-firm" process. This is an odd phenomenon, given that almost every supply chain is really a supply network that involves multiple parallel nodes. For example, an automotive manufacturer often buys the same part from multiple suppliers, moves that part with various transportation vendors, and ultimately sells a car at multiple retail points. These are complex inter-firm structures in which a product's demand volatility diffuses in parallel as well as serial dimensions. This observation raises an important question: does BWE work in the same way when considered from the inter-firm perspective as it does in the common intra-firm context? This is not just a theoretical question, of course. There are many suggested technological, mathematical, and process solutions for BWE, generally based on the intra-firm view. If BWE is indeed different in the inter-firm context and aligns more closely with the real world, then the existing understanding of BWE and associated solution set may need to be revised.

Evolving our understanding of BWE is the focus of a forthcoming paper from Nikolay Osadchiy (Emory), William Schmidt (Cornell), and Jing Wu (Chinese University of Hong Kong), which provides a novel contribution to the analysis of the issue by looking at it from the inter-firm perspective. In other words, their paper examines the collective effect of demand distortion and variance amplification mechanisms on the BWE in supply networks. Specifically, the authors ask "whether demand distortion, i.e., intra-firm BWE, leads to variance amplification upstream in the supply network." If not, is BWE not present because of the statistical aggregation in demand that occurs at the network level or because changes in customer make-up (i.e., the "customer portfolio") reduce or even eliminate the effect.

The second phenomenon, customer make-up, may surprise some supply chain professionals, but the authors point out that there is anecdotal evidence that in many cases a less volatile customer can "smooth out" a more volatile one:

For example, about 85% of orders at Dell are for corporate customers. Retail orders coming through the Internet can be fulfilled quickly even if demand is highly volatile because the corporate orders can be shifted slightly to absorb variability in retail customer demand. In a second example, when Hertz was a wholly-owned subsidiary of Ford Motor Company, 40% of some models were sold to Hertz. This arrangement allowed Ford to use the Hertz volume to fill in the valleys in demand when retail sales were slow.

These examples suggest that demand patterns can be an important characteristic of a customer base, one that can influence whether or not BWE exists in a supply network. Indeed, the authors speculate that suppliers may actively adjust their customer portfolio in response to potential BWE, which could make the customer portfolio serve as an organic demand risk hedge within a complex inter-firm ecosystem.

The Study

To test their ideas about the inter-firm BWE, the authors collected buyer-seller relationship data from the extensive FactSet Revere database. The data set covers the period from Q2 2003 to Q4 2015 and includes only relationships identified as customers or suppliers (while excluding other types such as competitors and partnerships).

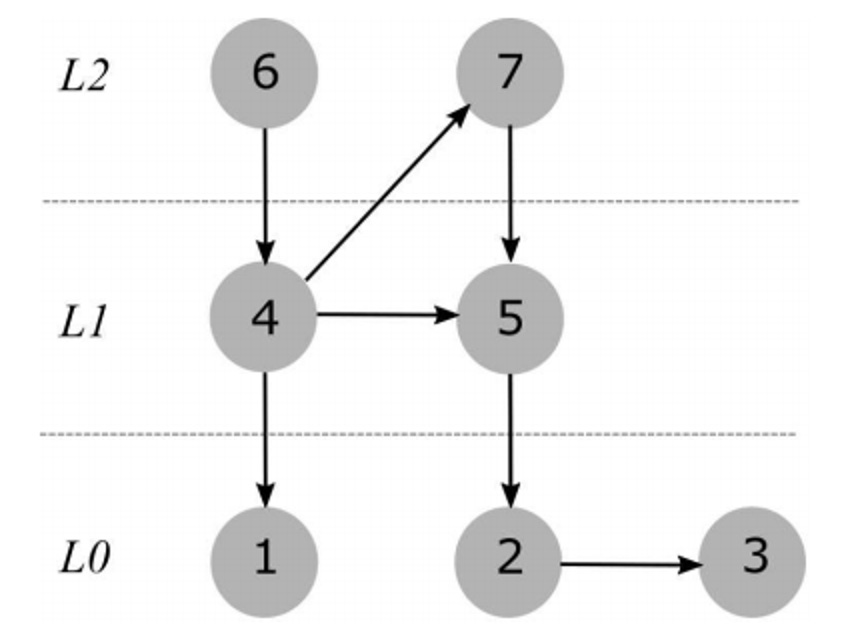

For each year in the data set, the authors assigned a measure of absolute position to each firm in the network, which they call a "measurement layer." For each firm, the layer is defined as the "shortest path distance from that firm to end consumers or final demand." Firms serving the final consumer demand are assigned to layer Layer 0 ("L0").

All L0 firms came from the consumer staples or consumer discretionary sectors. Layer L1 contains firms that are one directed link away from any firm in L0, the direction of a link is towards L0; L2 contains firms that are two links away from L0, and so on. The number of links is determined by the shortest path from a firm to L0. As Figure 2 below illustrates, firm 4 has multiple paths to L0. Because the shortest path has a length of one, firm 4 is assigned to L1.

On average, an L0 firm in the data set has about 4 reported customers, but it is important to note that a firms' customers are not necessarily located strictly downstream. As illustrated in Figure 2, customers can be located in the same layer. For example, firm 4 is located in L1 but supplies firm 5, also in L1. Indeed, it also supplies firm 7 which is located in L2.

Figure 2: Supply network levels. (Source: Authors)

As the authors note:

A Layer is a global measure that reflects the structure of the entire network in a conservative fashion. It induces an ordering between firms by their position in the supply network. For example, "a firm in L2 can have customers that are located in L1 or above, but never in L0. Thus, that firm is definitely more upstream than any rm in L1. Because Layer is defined by the shortest path, it reflects informational proximity to final demand; the latter is particularly relevant for information transmission and the BWE. From a logistical perspective, a higher layer in the supply network corresponds to more links in the logistical chain from a firm to final consumers.

Though the supply network collected by the authors can be deep (reaching a maximum number of 9 layers in 2007, 2008, and 2015), more than 70% of firm-year observations are concentrated in layers L0-L2, and approximately 85% are in layers L0-L3.

With their network models built, the authors calculated the degrees of (a) demand volatility (DV) and (b) BWE present in their entire sample of manufacturers, transportation, warehousers, wholesalers, and retail trade firms in the network.

In sum, the authors first placed every company in their data set within their "layered" network. Next, they used the financial and supply data in FactSet to calculate DV and BWE. Lastly, they looked to see if BWE did indeed increase with DV, as the theory predicts it should.

The Results

From their analysis, the authors reached two major conclusions. First, when there is demand volatility in a network, BWE is also present. This conclusion is consistent with classic BEW theory, of course, as well as with more recent research. However, the authors also found that moving back across the network did not increase the degree of BWE, a finding opposite of what the theory predicts. As the authors note, "we find no evidence that the downstream demand distortion translates to a commensurate amplification of demand variability at upstream layers of the supply network." In fact, "there is considerable evidence that DV can decrease upstream."

At this point the paper becomes more thought-provoking because the authors tested whether simple (a) demand aggregation or (b) changes made to customer mix could explain the absence of BWE upstream in the supply network. To do so they analyzed what happened to BWE when a supplier added, dropped, or swapped out a high DV customer. The authors found that "adds" resulted in an average reduction in the supplier's demand variability of between 5.8% and 11.4%. "Drops" resulted in reductions of between 3.3% and 16.4%, and "Swaps" result in reductions between 7.9% and 15.7%. Further testing negated the hypothesis that simple aggregation was the reason for the absence of BWE, a conclusion confirmed by interviews the authors conducted with over 20 companies in the U.S. and China. All of them, note the authors, "indicated that they indeed value and pursue (e.g., by offering better terms) customers with favorable demand patterns that help smooth out the aggregate demand."

Conclusions

The conclusion that complex supply networks not only mitigate but may actually eliminate BEW will be surprising to many supply chain professionals who take BWE as a fundamental truth of the field. Yet my experience as a former supply chain consulting partner who has researched and taught supply chain risk to MBA students also supports the conclusions of this paper. The most sophisticated companies understand the cost of risk that is embedded in various nodes of a supply chain network. It would be surprising to think that companies would not adjust their customer portfolios as a means of smoothing out demand volatility, and it is useful to see that intuition supported by empirical data.

A question these conclusions raise is whether there are any factors that allow some companies to execute this type of demand adjustment more than others. The authors speculate that one such factor may be asset utilization. The authors speculate that firms with high asset utilization should be using those assets at peak capacity (over time), which would make them less able to change customers in response to demand volatility. Firms with more asset flexibility may be those that are most able to use their network to hedge demand volatility.

In closing, the authors suggest that their work could lay the foundation for revisiting other fundamental supply chain questions such as "What is a good customer?" To that suggestion, I would add two more: What is a good forecast worth in terms of overall network demand volatility? and Would it make sense for suppliers to pay their least volatile customers a premium for their volatility-reducing value?

Analyses of network-level demand volatility are often too theoretical and have not received enough attention in empirical supply chain research. One can hope that the line of research extended with this paper will lead others to follow, giving us an enhanced understanding of the complex forces that shape demand and supply in today's complex global networks.

The Research

Osadchiy, Nikolay and Schmidt, William and Wu, Jing, The Bullwhip Effect in Supply Networks (August 30, 2018). Forthcoming in Management Science, Available at SSRN: https://ssrn.com/abstract=3241132

The authors provide another summary of their research in MIT Sloan Management Review here.