COVID-19 has changed supply chain risk

The pandemic should change how we calculate and manage supply chain risk costs across almost every global region and business sector

[In response to my cost of risk post on Monday, a reader asked how the COVID-19 pandemic fits into my CoR framework. My response is below. - CA]

I recently published a post summarizing extensive research I have undertaken to understand how risk creates cost in any supply chain. My work is different from most other supply chain risk research in that I am concerned with how risk creates real and present costs in supply chains and not a hypothetical future cost, e.g., that of a temporary disruption such as a weather-related event. The origin of my research goes back to when the CPO of a global cosmetics firm asked me to help him decide if a $1M consulting project to improve forecasting was worth the investment. I spoke with several of his direct suppliers, and all were charging my client a "risk surcharge" that ranged between 5-10% and was driven solely by their notoriously bad product launch forecasts. It was clear to me that on a direct spend of over $6B, my client's direct-spend "cost of risk" was a substantial, yet almost completely invisible and unmanaged, cost of doing business every day.

This experience started me on a road different from most supply chain risk work. I wanted to look at risk more from the point of view of an active stock trader, managing the risk of every transaction, and less as an insurance underwriter, worried about a low-probability event.

In last week’s post, I explained that every product has one price but two costs: the cost of the thing and the cost of the risk inherent in its production/delivery. Moreover, those costs are present each day that the supply chain operates and exist whether or not the supply chain is ever disrupted. They are inherent to the design and its operation, and this should be a subject of continuous quantification and management. This last point is one some people may find hard to understand and accept. Because we typically think of risk from the insurer's perspective, it can be challenging to understand that the moment any risk is introduced to a supply chain a cost is also introduced that is a direct function of the underlying uncertainty.

As I also mentioned in Monday’s post, many major CoR drivers exist in economic form before they exist in financial form. The point relevant to any analysis of COVID-19's impact on supply chains is that (a) economic costs can convert into financial costs, and that (b) this conversion has four features that can be observed and verified time and again.

Feature 1: All major risk cost conversions are generally predictable, i.e., no major shift of a risk cost driver from economic to financial has occurred without warning. I liken the conversion precursors to ticks on a seismograph before a major earthquake; if you pay close enough attention, no major conversion should ever be a surprise.

Feature 2: The moment of conversion is specifically unpredictable but generally predictable; moreover, it is usually sooner than most pre-conversion models predict. Once the seismograph ticks become steady, a conversion is inevitable. We may not be able to say exactly when it will happen, but we can estimate it better and better as the intervals of the precursors decrease and their magnitude increases. Generally speaking, risk models tend to overestimate the time left before conversion, because the models are typically based on hypothetical conversion scenarios and not readings of the actual precursors in the field.

Feature 3: The cost of conversion is always higher than predicted. Whatever you think the conversion will cost, it's probably wrong and most likely by a wide margin of error. Take your worst-case scenario and make it much worse to approximate what probably will happen when the conversion finally arrives.

Feature 4: Conversions are typically permanent, i.e., no major driver of supply chain CoR has moved back in modern times from the financial column to economic column. Once a CoR driver "flips," it usually stays flipped. Counterfeiting, terrorism, and climate change, for example, all made the conversion in past decades and all remain financial CoR drivers to this day.

As with other CoR conversions such as the Great Recession and climate change, the COVID-19 conversion of pandemic risk from economic to financial follows the same four features as outlined below:

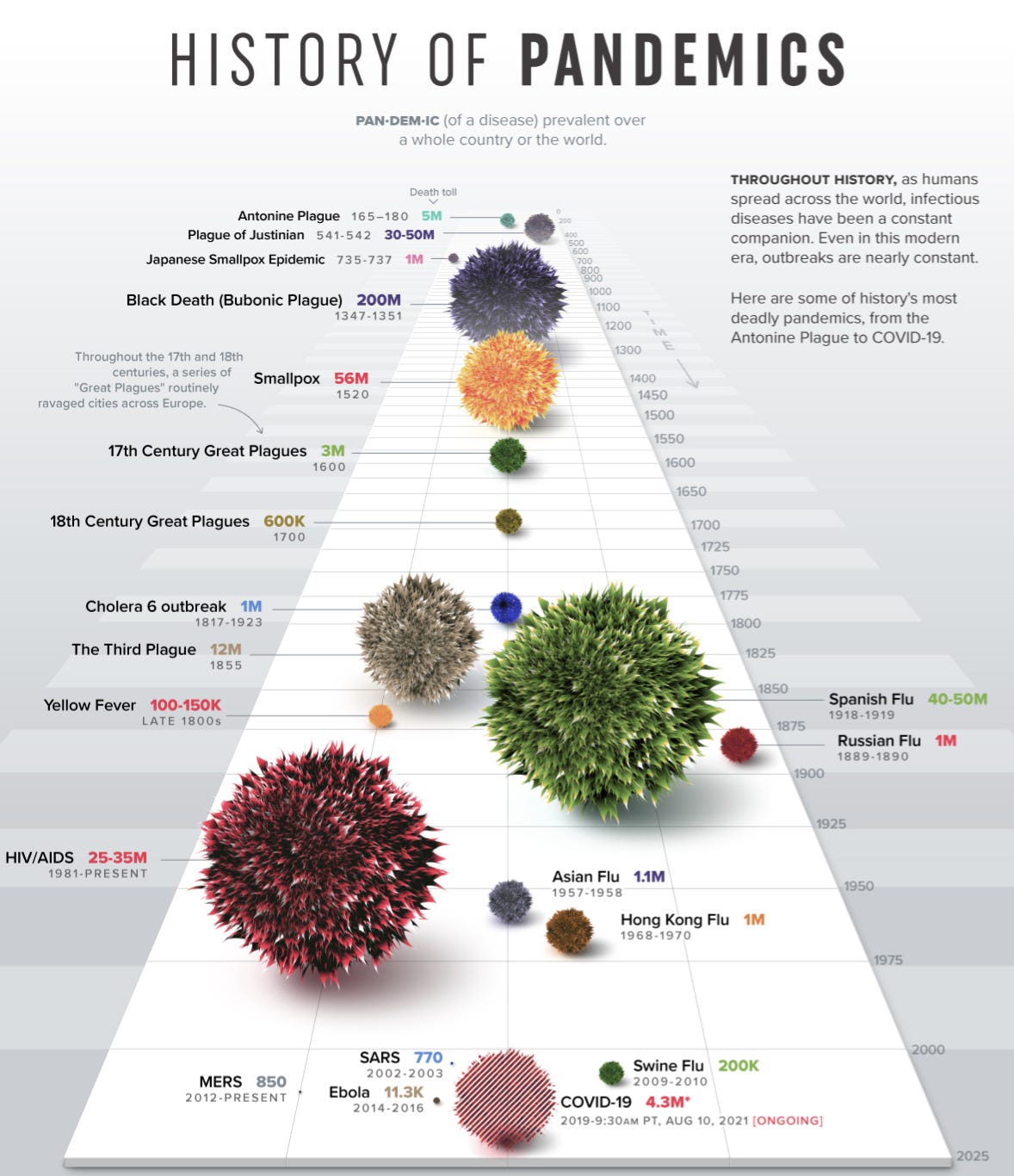

1) The idea that sooner or later pandemic risk would convert should have been there for anyone who was looking, as this sample of a great visualization from the Visual Capitalist suggests:

2) We could not predict COVID-19 would strike in 2020, but a look at the SARS-MERS-Swine Flu clustering was an indicator that the moment of conversion was probably getting closer.

3) The cost of the COVID-19 will far exceed what most supply chain managers had in any of their worst-case SCRM models.

4) Not one scientist with whom I have spoken believes that COVID-19 is a “once in a century” event. On the contrary, they believe that we are now in a world where such events will be a regular occurrence. However, much like financial crises, we will always be fighting the last outbreak, and it is highly likely that among the manageable epidemics we will continue to see catastrophic pandemics like the one we are living through today.

The point of this post is that every supply chain operator should understand that a fundamental cost of risk driver conversion is taking place during the COVD-19 outbreak and not just a months-long disruption. It will be necessary to revise all CoR models from this day forward to take into account the fact that pandemic risk is no longer an invisible economic CoR factor but a very real financial CoR driver that must be calculated, factored into any supply chain design, and managed actively. Moreover, I use the term "supply chain" in the broadest sense of the term, since this conversion applies to all social and business supply chains, from food to health care to education. That is not a happy thought, but it is the reality supply chain strategists and managers must confront once the crisis passes and they look toward the future.